While other financial sectors race ahead with 67% AI adoption, mortgage lenders lag just 38%—yet early adopters are already processing loans 40% faster. If you’re still relying on traditional methods, discover why the competitive gap widens every quarter and what it means for your business.

Key Takeaways:

The mortgage industry stands at a crossroads. While other financial sectors race ahead in implementing artificial intelligence, mortgage lenders find themselves significantly trailing behind. This technological gap presents both challenges and unprecedented opportunities for loan officers willing to act decisively.

The numbers tell a stark story about AI adoption across financial services. According to recent industry surveys, 38% of mortgage lenders reported using artificial intelligence in 2024, up from 15% the previous year. Yet this progress pales in comparison to other financial sectors, where adoption rates have soared well past the halfway mark.

Financial services have broadly reached 67% AI implementation, with investment banking leading at 58% and insurance companies showing rapid acceleration, with adoption rates reaching 76% for generative AI capabilities. This disparity highlights the mortgage industry's conservative approach to technological innovation, creating a landscape where early movers can establish significant competitive advantages. Autonomous Growth specializes in helping mortgage professionals bridge this technology gap through AI-powered marketing solutions designed specifically for loan officers and mortgage brokers.

The gap becomes even more pronounced when examining individual loan officers' adoption rates, which remain substantially lower than institutional implementation rates. While lenders themselves slowly adopt AI tools, the producers who actually generate business lag even further behind, creating multiple layers of opportunity for those ready to act.

The mortgage industry's hesitation to adopt AI stems from deeply rooted structural challenges that set it apart from other financial sectors. Understanding these barriers helps explain why the opportunity exists and why it will persist for forward-thinking professionals.

Mortgage companies operate within one of the most heavily regulated environments in financial services. The fragmented regulatory landscape, with its patchwork of state and federal AI laws, creates significant compliance concerns that often paralyze decision-making. Lenders worry about non-compliance with stringent regulations, data security vulnerabilities, and the potential legal ramifications of automated decision-making processes.

These compliance fears translate into increased costs and hesitation in implementing beneficial AI. Many organizations choose to maintain the status quo rather than navigate the complex regulatory requirements associated with adopting new technology. The result is an industry that prioritizes regulatory safety over competitive advantage, leaving substantial market opportunities for those willing to work within proper compliance frameworks.

Preserving Human Touch Influences Technology Strategy

The mortgage industry has traditionally operated on relationship-driven business models where personal connections determine success. Loan officers have built careers on face-to-face interactions, referral networks, and trust-based transactions that seem at odds with automated systems. This cultural emphasis on human relationships creates resistance to technologies perceived as impersonal or threatening to established practices.

However, this perspective overlooks how AI can strengthen relationship-building by handling routine tasks and enabling more meaningful client interactions. The most successful early adopters have discovered that AI amplifies their relationship capabilities rather than replacing them, allowing for faster response times and more personalized service delivery.

Many mortgage companies struggle with outdated technology infrastructure that makes AI integration complex and expensive. Poor data integration between new AI tools and legacy systems leads to process disruptions, incomplete data transfers, and operational inefficiencies that can temporarily reduce productivity during implementation.

Staff resistance to workflow changes compounds these technical challenges. Inadequate preparation for new systems and insufficient training create additional barriers that many organizations prefer to avoid. These integration hurdles, while real, are temporary obstacles that forward-thinking companies successfully navigate with proper planning and execution.

While mortgage lenders grapple with adoption challenges, other financial sectors have adopted AI implementation at unprecedented rates, creating instructive contrasts that highlight the mortgage industry's untapped potential.

Investment banking firms have aggressively pursued AI adoption to gain competitive advantages in trading, risk assessment, and client service delivery. These organizations recognize that AI capabilities directly impact profitability and market position, driving rapid implementation across core business functions. The 58% adoption rate in investment banking demonstrates how quickly financial services can transform when leadership prioritizes technological advancement.

Investment banks use AI for algorithmic trading, fraud detection, portfolio optimization, and client relationship management. Their success stories provide blueprints for mortgage industry applications, particularly in areas like document processing, risk evaluation, and customer communication, where similar benefits apply.

Traditional banking and insurance companies in the broader financial services sector have reached approximately 67% AI adoption rates by focusing on improving customer experience and enhancing operational efficiency. Insurance is accelerating rapidly, with 76% adoption of generative AI capabilities. These sectors have successfully integrated AI into loan processing, claims management, customer service, and compliance monitoring without sacrificing regulatory requirements or customer relationships.

The success of banks and insurers in maintaining regulatory compliance while implementing AI solutions directly contradicts the mortgage industry's compliance concerns. These parallel financial sectors operate under similar regulatory frameworks yet have found ways to use AI benefits while meeting all legal requirements, proving that regulatory compliance and technological innovation can coexist successfully.

The mortgage professionals and companies that have adopted AI implementation are experiencing measurable improvements that validate the technology's potential impact on industry operations and competitive positioning.

A mid-sized mortgage lender successfully implemented a custom AI solution specifically designed for automated document review of unique loan products. This targeted application achieved 40% faster processing times while significantly reducing manual errors that previously required costly corrections and delays.

The success came from focusing AI implementation on specific, well-defined tasks rather than attempting broad transformation across all operations. By automating repetitive document analysis and data verification processes, the lender freed up staff time for higher-value activities while improving accuracy and speed throughout their operation.

AI-powered automation has demonstrated remarkable capability to reduce data entry errors by up to 90% and boost compliance accuracy by up to 85%. Advanced AI systems can achieve very high accuracy, with 99.5%+ often required for fully automated loan decisioning. These improvements translate into substantial cost savings and risk reduction for mortgage operations that traditionally rely on manual data processing and verification.

The high accuracy rates achieved by properly implemented AI systems far exceed typical human performance on repetitive tasks. This accuracy improvement reduces costly mistakes, minimizes compliance issues, and creates more reliable operations that benefit both lenders and borrowers throughout the mortgage process.

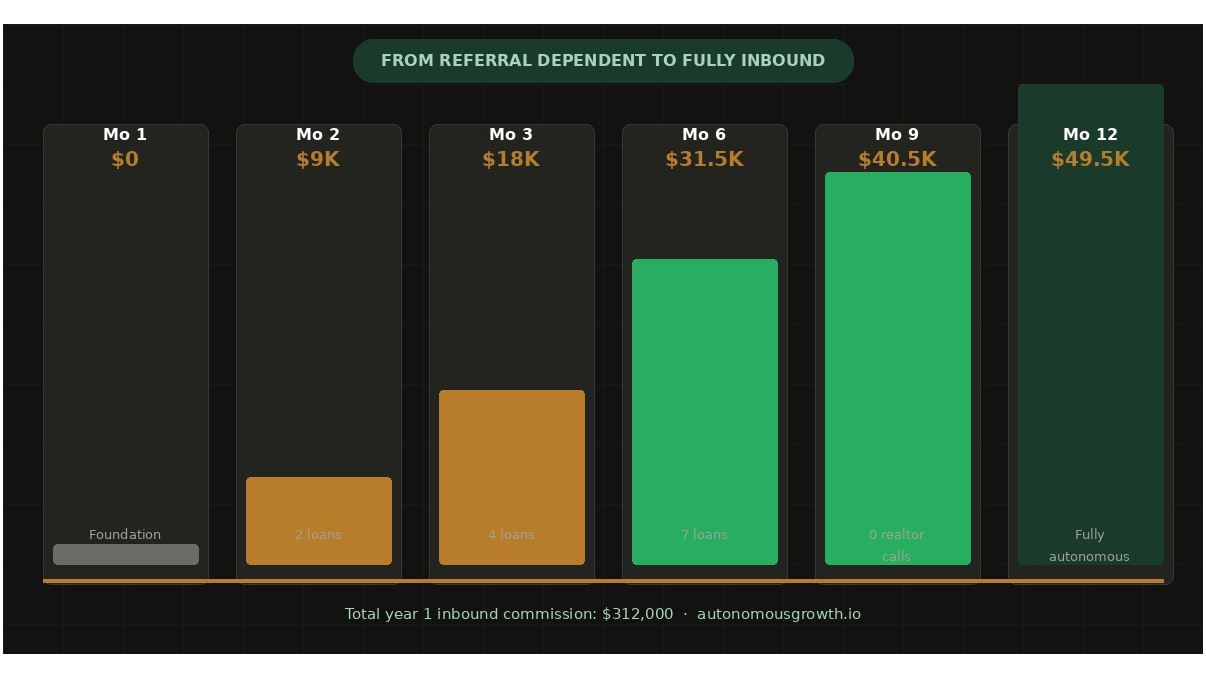

Advanced AI agent platforms can now handle over 20,000 automated calls per day, with the capacity to scale to 30,000, and manage initial customer inquiries, qualify prospects, and schedule appointments without human intervention. This capability allows loan officers to focus entirely on qualified prospects and relationship building rather than spending time on initial lead screening and administrative tasks.

These AI agents operate 24/7, ensuring that potential clients receive immediate responses regardless of time zones or business hours. The system captures leads that would otherwise be lost to delayed response times while providing consistent, professional interactions that improve brand reputation and customer experience.

The mortgage industry's slow AI adoption creates a unique environment where early movers can establish competitive advantages that become increasingly difficult for followers to overcome. These advantages compound over time, creating sustainable market positions for professionals willing to act decisively.

Companies that completely avoid AI engagement risk falling behind as the technology improves customer offerings, helps originators provide more suitable products, and significantly accelerates processing times. The competitive gap between AI adopters and traditional operators continues to widen each quarter, making delayed adoption increasingly costly in terms of market share.

Despite rising adoption rates, mortgage origination costs often remain high, sometimes exceeding $12,000 per loan, suggesting that fragmented decision-making and 'bolt-on' technology solutions, rather than integrated AI systems, are hindering the industry's potential to reduce costs. Early adopters who implement strategic AI approaches position themselves to capture market share from competitors struggling with high operational costs and slower service delivery.

The window for establishing first-mover advantages remains open, but industry trends suggest this opportunity will not persist indefinitely as adoption rates accelerate and competitive pressures mount across all market segments.

Autonomous Growth helps mortgage professionals capitalize on current AI adoption gaps through marketing automation designed specifically for the lending industry.