Over half of Australians die without a valid will, but even those who have one face a shocking reality: family provision claims succeed 74-77% of the time, allowing people you deliberately excluded to challenge your wishes. Are you making these costly mistakes?

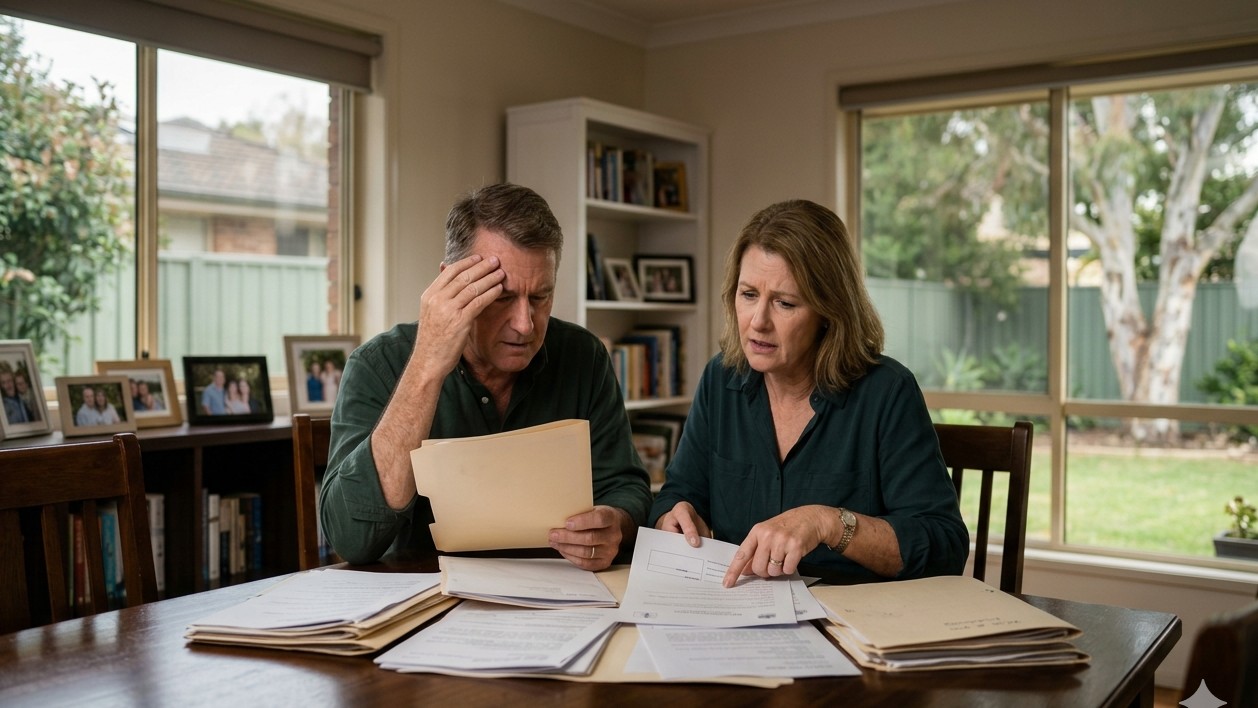

The most devastating inheritance mistake isn't about who gets what - it's failing to plan at all. When families find their loved one's estate heading to court instead of following their wishes, the financial and emotional cost can destroy relationships and drain inheritances for years.

Approximately 48% to 52% of Australians die without a valid will, leaving their assets to be distributed according to state intestacy laws. This staggering statistic reveals the most common inheritance mistake plaguing Australian families: inadequate estate planning.

When someone dies intestate, their estate doesn't simply go to their closest family member. Instead, a rigid legal formula determines who inherits what, often creating outcomes that contradict what the deceased would have wanted. Professional estate planning services can prevent these unintended consequences by ensuring wills are properly structured and legally valid.

The consequences extend far beyond disappointing beneficiaries. Dying intestate creates significant additional effort, expense, and stress for families during an already difficult time. The legal process for determining asset distribution can take months or years, freezing access to funds when families need them most.

Inexpensive DIY will kits might seem like a practical solution, but they're designed for very simple situations. Modern Australian families often have complex structures that basic templates cannot adequately address, leading to errors, invalidity, or unclear instructions.

More than 10% of Australian families are blended, creating inheritance-planning complications that standard wills cannot address. These complex structures frequently lead to disputes over how to balance the interests of current spouses and children from previous relationships.

The challenge intensifies when considering step-children, half-siblings, and multiple sets of grandparents. A simple will might inadvertently exclude step-children or create unequal distributions that fuel family resentment for generations.

Superannuation assets do not automatically form part of a deceased estate. Without a valid binding death benefit nomination, the super fund trustee has discretion over who receives the benefit, potentially overriding the will entirely.

This creates a dangerous gap where significant assets - often representing the largest portion of someone's wealth - follow different distribution rules than the rest of their estate. Many families learn too late that superannuation has gone to an ex-spouse or estranged family member despite clear instructions in the will.

Business owners face particular challenges when personal and business wealth are intertwined. Company shares, partnership interests, and trust distributions require careful succession planning that goes far beyond basic will provisions.

Without proper business succession planning aligned with estate documents, valuable enterprises can face operational paralysis or forced sales at unfavourable prices, dramatically reducing the value of the inheritance for beneficiaries.

Even with a valid will, Australian families face another threat to inheritance: family provision claims. The Family Provision Act grants eligible persons - including spouses, de facto partners, and children - the statutory right to contest a will if they believe they haven't been adequately provided for.

Family provision claims have an alarmingly high success rate in Australia, with studies indicating up to 77% success rate in jurisdictions like Queensland. This means that most challenges to wills result in court-ordered changes to the deceased's intended distribution.

A real case illustrates this threat: a successful businessman's half-brother, not mentioned in the $2 million estate will, successfully challenged the distribution. The resulting two-year court battle consumed significant legal costs and emotional energy, ultimately forcing a settlement that contradicted the deceased's clear wishes.

The definition of "eligible persons" under family provision legislation is broader than many people realise. Ex-spouses, de facto partners, and adult children can all mount successful challenges, even when deliberately excluded from a will.

This legal landscape means that writing someone out of a will doesn't guarantee they won't receive an inheritance. Without proper estate planning strategies, excluded family members often receive substantial portions through court intervention.

While Australia doesn't impose inheritance tax, significant tax obligations can arise when beneficiaries deal with inherited assets. These hidden costs often surprise families who haven't planned for the tax implications of their inheritance strategy.

When inherited property or shares are sold by beneficiaries, the sale may trigger a substantial Capital Gains Tax liability. For assets acquired by the deceased on or after 20 September 1985, the tax applies to the growth in value from the original purchase date. For assets acquired before this date, the cost base is generally the market value as of the date of death, potentially resulting in significant tax bills for unsuspecting heirs.

Property that served as the deceased's main residence may qualify for the CGT exemption if sold within two years of death. However, beneficiaries may also qualify for a CGT exemption if they occupy the inherited property as their main residence. After the two-year window closes without meeting these conditions, partial exemptions or full CGT liability apply, potentially costing tens of thousands in unexpected tax.

Superannuation death benefits paid to non-dependants - which can include adult children - are subject to tax at 15% plus the Medicare levy on the taxable component. However, adult children can be classified as dependents for tax purposes if they meet specific criteria, such as financial dependency or an interdependency relationship with the deceased.

Many parents assume their superannuation will pass tax-free to their children, not realising that adult children may be classified as non-dependents for tax purposes unless they meet specific dependency criteria, regardless of their relationship or financial circumstances.

The narrow two-year window for CGT exemption on inherited main residences creates timing pressure that many families struggle to meet. Property markets, family disputes, or simple procrastination can push sales beyond this critical deadline, triggering substantial tax obligations.

Families dealing with grief and complex estate administration often find two years insufficient to make informed decisions about the disposal of property, especially when multiple beneficiaries must agree on timing and strategy.

Even properly drafted wills can become invalid or inadequate when life circumstances change. Major life events automatically affect will validity in ways that catch many families unprepared.

Under Australian law, marriage automatically revokes any existing will unless the will specifically contemplates the upcoming marriage. This means countless Australians unknowingly invalidate their estate planning on their wedding day.

The revocation is complete and immediate, leaving newlyweds intestate until they create new wills. For couples with significant assets or children from previous relationships, this creates a dangerous planning gap that could last months or years.

The birth or adoption of children, or acquiring step-children through remarriage, fundamentally changes estate planning needs. Outdated wills may fail to adequately provide for new family members or create unintended conflicts between generations of children.

Step-children face particular vulnerability, as they're not automatically provided for under intestacy laws in most states. Without explicit inclusion in updated wills, they may receive nothing despite being treated as family members during the deceased's lifetime.

The cost of addressing inadequate estate planning far exceeds the cost of proper professional advice. Court challenges, family disputes, and tax penalties can easily consume hundreds of thousands of dollars that should have gone to beneficiaries.

Professional estate planning involves coordinated advice from financial planners, lawyers, and tax advisers who understand the complex interactions between wills, superannuation, business structures, and tax obligations. This integrated approach ensures all aspects of wealth transfer work together seamlessly.

Regular reviews every 2-3 years or after significant life events ensure estate plans evolve with changing circumstances. Professional advisers can identify potential issues before they become costly problems, protecting both the estate's value and family relationships.

The investment in detailed estate planning typically represents a tiny fraction of the potential costs of getting it wrong, making it one of the most cost-effective financial decisions families can make.

Approved Financial Planners specialises in detailed estate planning strategies that protect Australian families from costly inheritance mistakes and ensure wealth transfers according to personal wishes.